The Quiet Harvest: Assam's Premium Agri-Food Export Window

Singapore's HC asks publicly for more Tezpur litchis. The supply chain cannot deliver. Here is why the gap exists and what it will take to close it.

0 of 10 sections read

On June 9, 2026, the Singapore High Commission posted a photo of HC Simon Wong with a basket of Tezpur litchis. The caption: “Enjoying very much my #Assam #tezpur #litchi. Many thanks to Hon CM @himantabiswa for introducing Singapore to this variety of sweet litchi. It is selling fast in Singapore. Export more please.”

The post collected 85,500 views and 2,000 likes on a verified diplomatic account, which makes it something more interesting than a courtesy tweet. Foreign missions do not publicly request additional stock of a perishable agricultural product unless they have buyers waiting.

Three days later, CM Himanta Biswa Sarma flagged off 500 kg of GI-tagged Piyaji litchis to Singapore from LGBI Airport’s cargo terminal. This followed 1,000 kg to Dubai on June 7 and 600 kg to Singapore on June 9, all routed through APEDA.

The Times of India covered the initial shipments, noting APEDA’s role and Assam’s broader agri-export push.

In volume terms, 1,500 kg of litchi is a small batch. What matters is the sequence that followed: a foreign diplomat asked publicly for more product, the CM responded with infrastructure commitments, and LGBI’s cargo numbers showed 15.1% year-on-year growth. As our logistics roadmap for Eastern India noted, cargo throughput at gateway airports sets the viability ceiling for perishable exports from the region. That ceiling just moved.

But demand without supply-chain capacity is just a headline. Assam has been here before, and the reasons the supply side failed last time have not all gone away.

Before the optimism, the cold water. Assam has been on the verge of an agri-processing breakout before. Each time, the same structural failures killed it.

Post-harvest loss eats the margin. India loses 6 to 15% of fruit output after harvest, per a 2022 NABCONS study commissioned by the Ministry of Food Processing Industries. In the NER, those numbers run higher. A pineapple from Barpeta that sits unrefrigerated for six hours after picking loses its export-grade quality. A litchi from Sonitpur that misses the pre-cooling window is juice-grade at best.

The cold chain gap is not about storage capacity. The National Centre for Cold Chain Development found in 2020 that India’s cold storage shortfall was 8%. The actual gaps: reefer vehicles (85% shortfall), packhouses (99% shortfall), ripening chambers (91% shortfall). Sathguru Management Consultants calculated that 30 to 40% of losses hit during transportation and marketing. The mile between farm and cold room is where value dies.

The cold chain crisis is not about cold rooms. India’s cold storage shortfall is just 8%. The actual bottlenecks: packhouses at 99% shortfall, ripening chambers at 91%, reefer vehicles at 85%. Every Assam agri-processing business plan that assumes cold-chain availability should read the NCCD 2020 data first.

FIGURE 1: INDIA’S COLD CHAIN INFRASTRUCTURE GAP

Capacity shortfall as % of required, by cold chain component. NCCD 2020. Cold storage shortfall is small; execution-chain shortfalls are severe.

Middlemen, not soil, are the constraint. An academic survey of ginger and turmeric growers in Karbi Anglong and Jorhat, published in 2023, ranked middlemen dependency and poor market infrastructure as the top two constraints, ahead of yield or quality. The aggregation layer between producer and exporter extracts margin at every stage and delivers no quality assurance in return.

Certification fails before the product does. India processes 2.2% of its fruit and vegetable output. The US processes 65%. China processes 23%. India is the world’s second-largest producer of fruits and vegetables. It is not the second-largest processor. The gap is institutional: the ability to certify, document, and consistently meet quality specifications that premium markets require.

The NER geographic penalty persists. A ginger consignment from Karbi Anglong to London routing through LGBI pays a logistics premium that the same product from Kerala does not. This has not disappeared. But LGBI’s growth has begun to change the arithmetic. We mapped this freight-cost penalty in detail in the East-NE logistics roadmap.

These are the reasons every previous agri-processing push stalled. The question worth asking is why this time looks different, and the answer is not in policy announcements. It is in freight manifests.

The failure history explains why previous attempts stalled. It does not explain away the present. Something changed: real consignments, measured in metric tonnes, reaching real markets.

Litchi: 1,000 kg to Dubai (June 7), 600 kg to Singapore (June 9), 500 kg to Singapore (June 12). Growers received 10% above domestic market rates, per APEDA.

GI-tagged Karbi Anglong Ginger: 21.2 MT to London, March 2026. First GI-certified fresh ginger from Assam to the UK. Separate 10 MT consignments each to Qatar, Oman, and Dubai.

GI-tagged Joha Rice: 25 MT to the UK and Italy. GI status since 2017. Major producing districts: Sivasagar, Jorhat, Golaghat, Dibrugarh, Lakhimpur.

Pineapple: 42 MT to Dubai, promoted at Lulu Group supermarkets in the UAE.

Kaji Nemu: 1.2 MT to London.

Black Rice: 100 MT to South Indian markets.

Organic Banana: 87 MT to Bihar.

FIGURE 2: ASSAM’S VERIFIED AGRI-EXPORT RECORD, 2025-26

Volume in metric tonnes, GI-tagged and organic consignments. Sources: CM Himanta Biswa Sarma (X, June 2026); APEDA press releases 2022-2026.

Every consignment used GI certification or organic status as the price lever. GI-tagged products travel with documentation that commodity produce cannot match, and that documentation unlocks the premium-price shelf. The Nitisagar Subsidy Calculator maps the capital investment incentives available under UNNATI 2024 and NEIDS for food processing units across Assam’s districts.

The consignments prove that demand exists and that Assam’s produce can reach it. What they do not yet prove is that the state can serve that demand at scale. That depends on what is being built on the ground.

On June 11, between the HC’s tweet and the Singapore flag-off, the CM posted the supply-side response.

“The future of Assam’s agriculture lies in creating more value.” Four processing units under MMUY, each in a district that maps to a specific crop cluster:

Lakhimpur: Pineapple Processing. Assam’s pineapple belt. The anchor facility for cold-chain aggregation and semi-processing. MSMEs evaluating juice, pulp, or dried-pineapple formats can co-locate around it.

Morigaon: Modern Rice Mill. Grading and certification hub for Joha rice export. Morigaon also sits in the Tata OSAT supply chain corridor that Gear Shift has tracked since Issue #1. No other district in Northeast India combines semiconductor packaging with GI-certified rice milling.

Tinsukia: High-Tech Mushroom Spawn Unit. Upper Assam, adjacent to major tea estates. Mushroom cultivation integrates with tea-waste composting. Targets the hotel and food-service sector.

Kamrup: Advanced Spice Processing Unit. The logistics hub. LGBI Airport access. This is the drying, grinding, and packaging node for ginger, turmeric, and chilli arriving from Karbi Anglong and the hill districts. The 2023 Karbi Anglong spice grower study recommended exactly this: a dedicated spices park with a formalised export channel.

Processing units, though, are only as useful as the cargo infrastructure that connects them to buyers. A spice processing unit in Kamrup with no reliable air-freight route to the Gulf is a warehouse with expensive machinery. The question is whether LGBI Airport can carry the weight.

Perishables need air freight. The CM’s June 12 cargo post puts the litchi story in its logistics frame.

FIGURE 3: LGBI AIRPORT CARGO VOLUME

Metric tonnes handled annually. Source: CM Himanta Biswa Sarma (X, June 12, 2026).

LGBI handled 33,555.99 MT in 2025-26, up from 29,155 MT. More cargo volume brings more airline slots, more ground-handling competition, and lower per-kilogram costs. Each reduces the NER geographic penalty described above.

The Singapore consignment travelled via Druk Air routed through Guwahati from Bhutan. That is an improvised routing, not a commercial solution. Direct perishable-cargo routes from LGBI to Singapore or Dubai would cut transit time and cold-chain risk for every NER agri-export.

As Gear Shift #3 noted in the context of semiconductor supply chains, Assam’s logistics infrastructure is building to industrial-grade specifications. Agri-processing exporters ride the same investments.

Growing cargo throughput solves the logistics constraint. It does not solve the compliance constraint. India has a recent, expensive example of what happens when the product is ready, the logistics work, and the compliance system fails anyway.

India’s mango export is the closest parallel to what Assam is attempting with litchi, ginger, and pineapple. It offers a template and a warning.

The template. India shipped 32,104 MT of fresh mangoes in 2023-24 at USD 60.14 million, up from 22,963 MT the previous year. GI-tagged Alphonso from Ratnagiri and Kesar from Gujarat command air-freight premiums to the US, UK, UAE, and EU. APEDA built the scaffolding: packhouses at origin, Agri Export Zones in producing districts, export facility centres at Ratnagiri and Malihabad. Net margins on premium Alphonso air-freighted to Europe run 15 to 30%.

The warning. In March 2026, Japan suspended all Indian mango imports. The reason was not pesticide contamination or product defect. Japanese inspectors found procedural lapses at India’s Vapour Heat Treatment facilities. The fruit was fine. The facility management was not. Japan had banned Indian mangoes once before, from 1986 to 2006, over fruit-fly concerns. It took 20 years to rebuild that market. The EU imposed its own ban in 2014 over phytosanitary failures, lasting seven months.

Japan’s 2026 mango suspension was triggered by procedural lapses at treatment facilities, not by pesticide residues or product quality. The GI tag does not protect against compliance system failures. One procedural lapse terminates a trade relationship built over decades. For Assam’s new export programmes, the CM’s instruction — “strict compliance with prescribed standards, including the scientific use of fertilisers and consistency in production practices” — is not boilerplate. It is the mango case study applied.

Processed formats as insurance. Industry analysis increasingly favours processed mango products for a specific reason: processed formats carry lower phytosanitary risk (no fruit-fly vector), longer shelf life, cheaper sea-freight, and year-round revenue rather than a seasonal window. For Assam’s pineapple, ginger, and litchi sectors, the processed format is the more defensible commercial position.

The mango story is a national cautionary tale. Assam has a local one that is equally instructive, and it has been unfolding for 180 years.

Tea is the one local precedent that agri-processing investors can study directly.

The numbers. Assam produces half of India’s tea. India exported 255 million kg in 2024, passing Sri Lanka as the world’s second-largest tea exporter. Orthodox tea auction sales at Guwahati doubled in 2025-26 after the state raised the orthodox production subsidy from Rs 10 to Rs 15/kg.

The concentration risk. Iran imports 28 million kg of Indian orthodox tea annually. 24 million kg originates from Assam. The Iran-Israel conflict disrupted shipments, froze payment settlements, and cratered auction prices. Shipments worth Rs 150 crore were directly affected. Approximately 41% of India’s tea exports pass through the Strait of Hormuz.

Sri Lanka, another major orthodox tea exporter to Iran, did not see a comparable price decline during the same conflict period. Analysts attribute this to more diversified export strategies. Assam’s litchi, ginger, pineapple, and lemon export programmes are each at the stage where market diversification is still easy to build in. It becomes exponentially harder after concentration sets in.

What new sectors can learn from this. Market concentration is the export sector’s primary long-term risk. The Iran dependency took decades to accumulate. Tea’s secondary lesson is about the certification premium: the GI tag formalised a claim that the product had already earned through consistent quality. The same sequence applies to Tezpur litchi, Karbi Anglong ginger, and Kaji Nemu. The GI tag is the institutional recognition of an existing quality advantage, not the beginning of one.

Compliance risk and market concentration are the threats. The opportunity sits in the gap between what Assam’s farmers receive and what consumers in Mumbai, Dubai, and London pay.

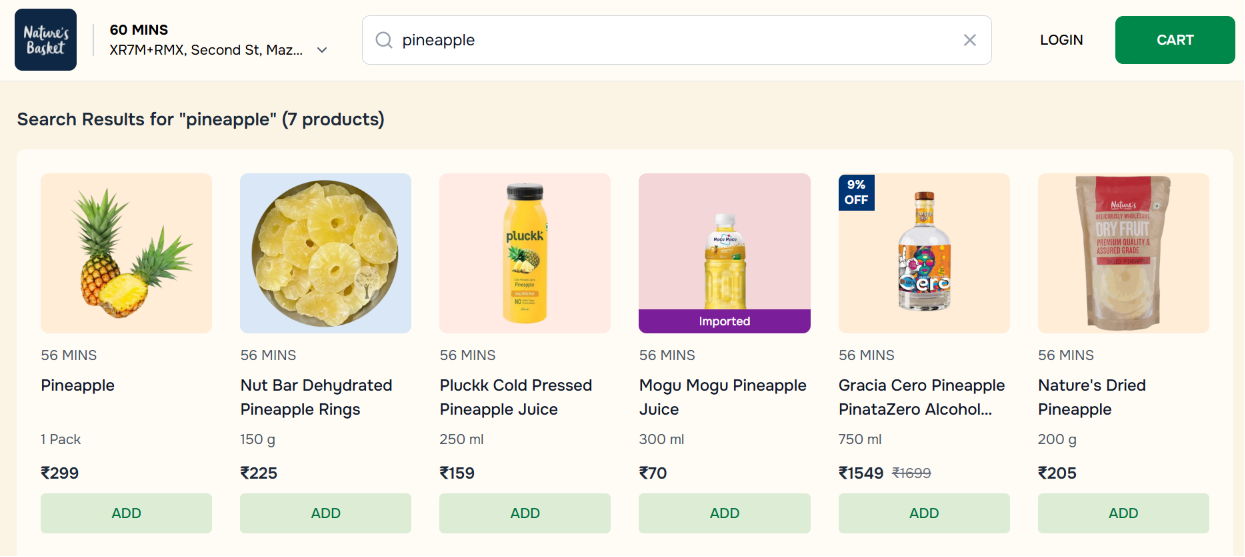

A single pineapple lists at Rs 299 on Nature’s Basket, the premium grocery chain present across tier-1 metros. The farmgate price in Assam, where the state produces 18.08% of India’s total pineapple production value, is a fraction of that.

But the Rs 299 whole pineapple is actually the lowest-margin product on the shelf. Search “pineapple” on Nature’s Basket and the full value-addition spectrum becomes visible in a single screenshot:

A whole pineapple at Rs 299 weighs roughly 1 to 1.5 kg. Dehydrated pineapple rings sell at Rs 225 for 150 grams, which translates to Rs 1,500 per kg of finished product. Dried pineapple sells at Rs 205 for 200 grams, or Rs 1,025 per kg. Cold-pressed pineapple juice sells at Rs 159 for 250 ml. Each of these processed formats was made from the same raw fruit that trades at Rs 30 to 50 per piece at Assam’s farmgate. The dehydrated rings represent a roughly 30x to 50x farmgate multiple. The drying, slicing, and packaging step is not a value-add. It is the primary value creation event.

This is the shelf that Assam’s pineapple processors are competing for. The Lakhimpur processing unit under MMUY, if it produces dried rings or juice concentrate rather than shipping fresh fruit, enters a market where the per-kilogram retail price is an order of magnitude above the commodity price. The MSME opportunity is not in growing more pineapples. It is in what happens to the pineapple between harvest and shelf.

APEDA has already placed Assam pineapples in Dubai’s Lulu Group supermarkets. The APEDA Chairman said specifically: “We need to focus on promoting pineapple in processed form in the Gulf countries. It will help farmers in better price realisation.” A fresh pineapple has a narrow harvest window and a cold-chain-dependent shelf life. A juice concentrate trades year-round and ships by sea.

For GI-tagged spices, the margin is sharper. Meghalaya’s Lakadong turmeric, a comparably GI-tagged NER product, sold at Rs 179/kg dried and Rs 267/kg powdered in 2024. The raw commodity price is a fraction of either number, even though the underlying crop is identical. The processing step changes the addressable market entirely.

The 8.3x multiple on Lakadong turmeric between raw farmgate and powdered export price is not a special case. It is the normal arithmetic of processing. The Assam MSME sector is concentrated at the farmgate end of this chain.

FIGURE 4: FARM TO SHELF — WHERE VALUE ACCRETES

Value multiple at final retail/export price versus farmgate base (1x). Sources: Nature’s Basket (June 2026); ICRIER Turmeric Report, Meghalaya 2024; trade cross-reference data.

The price gap is clear. The processing step captures most of the value. The question is whether anyone has proven this works at national scale with a similar crop basket. One country has, and its climate is almost identical to Assam’s.

The better comparator for Assam’s agri-processing ambition is not Maharashtra or Andhra. It is Thailand. Similar monsoon climate, similar tropical crop basket (pineapple, mango, ginger, lychee, jackfruit), and a country that chose processing over raw commodity export as national strategy.

Thailand’s agri and agro-industrial exports hit USD 52.19 billion in 2024, up 5.9% year on year. Food processing generates approximately USD 10 billion annually and accounts for up to 28.3% of GDP. More than half of the country’s 28 million tonnes of annual processed food output is exported.

Thailand and Assam grow the same crops in broadly similar climates. Thailand’s food processing sector is 28.3% of GDP. India’s is roughly 8-9%. The difference is not agronomic. It is a policy choice made four decades ago to invest in value addition over raw commodity export.

The route was not raw material abundance. An analysis of the Thai model identifies five pillars: directed policy with jointly set targets, value addition as the primary lever, stable policy continuity, private-sector-led execution, and government focus on hard infrastructure. The government enabled. The private sector executed.

FIGURE 5: TWO COUNTRIES, SAME CROPS, DIFFERENT OUTCOMES

Agri-processing comparison, Thailand vs. India. Sources: Freshdi Events / Thailand Board of Investment 2024; USDA GAIN TH2025-0030; Kuey Journal mango processing study.

Dried mango as product innovation. Thailand did not export fresh mango and stop. OECD-FAO analysis tracked Thailand’s introduction of dried mango, freeze-dried slices, and mango chips that penetrated Japan, Korea, and Australia on shelf stability and standardised retail packaging. South Korea alone imports 1,800 tonnes of Thai Nam Dok Mai mangoes annually. Thai canned mangoes account for 59% of global canned mango exports. India has 40% of global mango output and lags significantly in product diversification beyond pulp.

For Assam, the takeaway is specific. The crop is not the competitive advantage. The processed format, the standardised pack, and the year-round supply chain are the competitive advantage. A Tezpur litchi preserve, a Bhut Jolokia sauce in a branded 100 ml bottle, a Kaji Nemu cold-pressed juice in an export-compliant pack can reach a Japanese convenience store without the phytosanitary complexity of fresh-fruit export.

The model exists. The question is where in Assam the raw material, the processing infrastructure, and the logistics converge district by district.

Tezpur Litchi (Sonitpur). GI tag: 2015. Production from approximately 3,000 bearing trees. International demand exceeds supply. MSME opportunity: packaging, cold-chain aggregation, pulp preservation.

Karbi Anglong Ginger (Karbi Anglong). GI tag: active. 21.2 MT to London, March 2026. MSME opportunity: dried ginger, powder, essential oil extraction.

Kaji Nemu (Multiple Districts). GI tag: active. 1.2 MT to London. MSME opportunity: cold-pressed juice, preserved lemon, fragrance inputs under the EU-India Blue Valley Cluster launched in Guwahati, June 2026.

Bhut Jolokia (Multiple Districts). GI tag: active. Premium pricing in European and North American specialty channels. MSME opportunity: dried whole, powder, oleoresin, hot sauce.

Pineapple (Kamrup, Nalbari, Barpeta, Hill Districts). 18.08% of India’s pineapple production value. 42 MT to Dubai. Processing unit under construction in Lakhimpur. MSME opportunity: juice, canned slices, dried rings.

Joha Rice (Upper and Central Assam). GI tag: 2017. Sivasagar, Jorhat, Golaghat, Dibrugarh, Lakhimpur. 25 MT to UK and Italy. MSME opportunity: milling, grading, vacuum packaging.

MSME entry points. Cold-chain pre-cooling units (50-200 MT) near Sonitpur, Lakhimpur, or Karbi Anglong under PMFME or APEDA facilitation. Certified processing and packaging: APEDA’s January 2026 Guwahati conclave confirmed the gap is NPOP certification and export-compliant packaging, not product quality. Supply-chain services (traceability, quality testing, export compliance for FPOs and grower groups) are scalable at sub-5 crore investment.

For MSMEs evaluating any of these sectors, the Nitisagar Subsidy Calculator can model the capital investment incentives available under UNNATI 2024 and NEIDS for a food processing unit in any district in Assam.

Singapore’s HC asked for more litchis. Japan’s mango ban shows what happens when compliance fails. Tea’s Iran dependency shows what market concentration costs in a single geopolitical season. Thailand’s processed food sector shows what the same crop basket produces when value addition is treated as the primary activity.

Assam has product diversity, four new processing units under construction, and a cargo airport growing at double digits. What it needs is an MSME layer that builds processed formats, maintains compliance systems, and diversifies across markets from the start.

Don't miss policy updates

Get the latest intelligence on industrial schemes, subsidy disbursements, and policy shifts across Northeast India, delivered to your inbox.